Being financially unbiased means having sufficient passive earnings to cowl your important or desired residing bills. A typical guideline is to goal for a web value equal to 25 occasions your annual bills, typically used as a baseline for reaching monetary independence. Nonetheless, this strategy is overly simplistic as a result of it relies on the composition of 1’s web value.

In case your web value consists completely of liquid, income-producing belongings, 25 occasions your bills ought to suffice. But when a lot of it’s tied up in a primary residence or illiquid private investments, you might not be capable to generate sufficient passive earnings or readily promote belongings for true monetary independence. Liquidity and money move are paramount for retirement.

For these retiring on the conventional age of 65, a web value of 25X your annual bills, supplemented by Social Safety, is normally enough for a cushty retirement. Nonetheless, the 25X rule turns into extra precarious for these in search of early retirement. Longer time horizons, inflation, and life-style modifications—like rising households—can shortly erode a seemingly ample web value.

Could not Keep Absolutely Retired For Lengthy On 25X Bills

Once I revisited my funds after a 2013 financial consultation, I used to be reminded of the constraints of the 25X rule for reaching FIRE (Monetary Independence, Retire Early).

Though I retired in 2012 at age 34 with a web value of roughly 38 occasions my annual bills, I couldn’t maintain full retirement past 18 months. The problem lay within the composition of my web value—a lot of it tied up in my major residence—and the rising prices of sustaining a rising family. These elements made early retirement way more advanced than I had initially anticipated.

My unique plan was to embrace an easier life with my spouse on my grandparents’ farm in Waianae, Oahu. The imaginative and prescient was idyllic: we’d supply most of our meals from the land and reside comfortably on $80,000 a yr. Nonetheless, detaching ourselves from San Francisco, a metropolis we’ve referred to as dwelling since 2001, proved troublesome. Life pulled us in a unique course.

Our journey took an excellent greater flip with the births of our kids in 2017 and 2019, additional anchoring us to San Francisco. The imaginative and prescient of a quiet life on the farm shifted to balancing the calls for of elevating a household in one of the costly cities on this planet. Early retirement, it turned out, required greater than a excessive web value—it demanded higher money move and a willingness to adapt to life’s surprising turns.

Why A Internet Price Equal To 25X Annual Bills Is Not Sufficient To Retire Early

In the present day, our web value is even higher than the 38X bills we had in 2012. But, I do not really feel financially unbiased as a result of our passive earnings does not totally cowl our present residing bills.

We had exchanged a considerable amount of productive investments producing passive income for a house that, though paid off, requires ongoing bills corresponding to property taxes, upkeep, and utilities—prices that shares and bonds don’t have.

My aim now could be to recoup the productive investments we allotted to our dwelling over the subsequent three years.

Rollover IRA as a Case Research on Internet Price Composition

Let’s take my rollover IRA as a easy instance of why 25X annual bills falls brief as a retirement web value goal. 25X is the inverse of 4%, the secure withdrawal price popularized within the Nineties by Invoice Bengen, creator of the 4% Rule.

Think about my IRA had been my solely asset, with a stability of $1,300,000. Which means my whole web value consists of my rollover IRA, a 100% productive, income-producing asset.

Coincidentally, in keeping with a Northwestern Mutual survey from late 2023, this quantity aligns with what Americans believe they need to retire comfortably. Let’s assume I reside off $40,000 a yr in bills. If we multiply $40,000 by 25, that equals $1,000,000, suggesting I may very well be financially unbiased.

Nonetheless, because of the sort of investments in my portfolio, it does not come shut to offering sufficient dividend earnings to reside on.

Low Passive Earnings As a consequence of a Development-Centered Portfolio

Ninety % of my Equities – $826,191- is allotted to progress shares. Microsoft presents the best dividend yield on this class at about 0.78%, adopted by Apple at 0.48%. This brings my common dividend yield throughout all my progress inventory holdings to round 0.2%, leading to simply $1,653 in dividends yearly.

The majority of my ETF holdings – $476,000 – is in VTI, the Vanguard Whole Inventory Market Index, which has a dividend yield of roughly 1.33%. Consequently, my blended yield for all the portfolio is round 0.6%, translating to about $7,800 in annual passive income.

With post-tax annual bills at $40,000, I’d want a portfolio roughly 6.4 occasions bigger—$8,320,000—to generate $50,000 in gross passive earnings to cowl bills after taxes.

It could appear extreme to wish an $8,320,000 portfolio to attain monetary independence with annual bills of $40,000. And it’s. Nonetheless, few individuals maintain their whole web value in liquid, income-generating belongings. For a lot of, their fairness isn’t as readily accessible as it’d seem.

Adjusting Your Internet Price Composition Isn’t At all times Straightforward

Astute readers might recommend that the simple technique to obtain monetary independence on a $1,300,000 web value is to regulate the funding composition: promote sufficient growth stocks and buy sufficient dividend shares or ETFs to generate $50,000 a yr, which might require a 3.8% dividend yield.

To do that, I must rejigger the vast majority of my portfolio. If my retirement portfolio was in a taxable brokerage account, I’d incur vital capital good points tax.

Thus, a rational investor with a taxable brokerage account is unlikely to promote shares they’re optimistic on until completely mandatory. As a substitute, they might proceed working or discover supplemental retirement income to assist their life-style. Any surplus money move may very well be directed towards dividend-paying shares or ETFs over time.

The Profit Of A Roth IRA For Early Retirees

Luckily for Roth IRA holders, investments will be traded inside these accounts with out triggering capital good points taxes. This enables for changes with out an instantaneous tax invoice, providing extra flexibility for portfolio restructuring. Therefore, for individuals who can construct a big sufficient Roth IRA for retirement, the pliability in repositioning your portfolio with out tax penalties is usually a nice profit.

For many who want to retire earlier than 59.5, you possibly can all the time withdraw your unique contributions tax- and penalty-free, no matter your age or how lengthy the account has been open. Since contributions are made with after-tax {dollars}, they’re not topic to penalties or taxes. After 59.5, you possibly can then withdraw earnings tax- and penalty-free, supplied your Roth IRA has been open for no less than 5 years.

For these planning to retire early, the method requires meticulous planning. After years of following a selected funding technique, you’ll want to regulate the composition of your portfolio to align along with your new monetary wants. On prime of that, you’ll face the problem of transitioning from accumulation to withdrawal, beginning with tapping into your contributions. This shift is simpler stated than accomplished and requires a transparent technique to keep away from pointless taxes, penalties, or liquidity points.

Housing Is A Excessive Share Of Internet Price

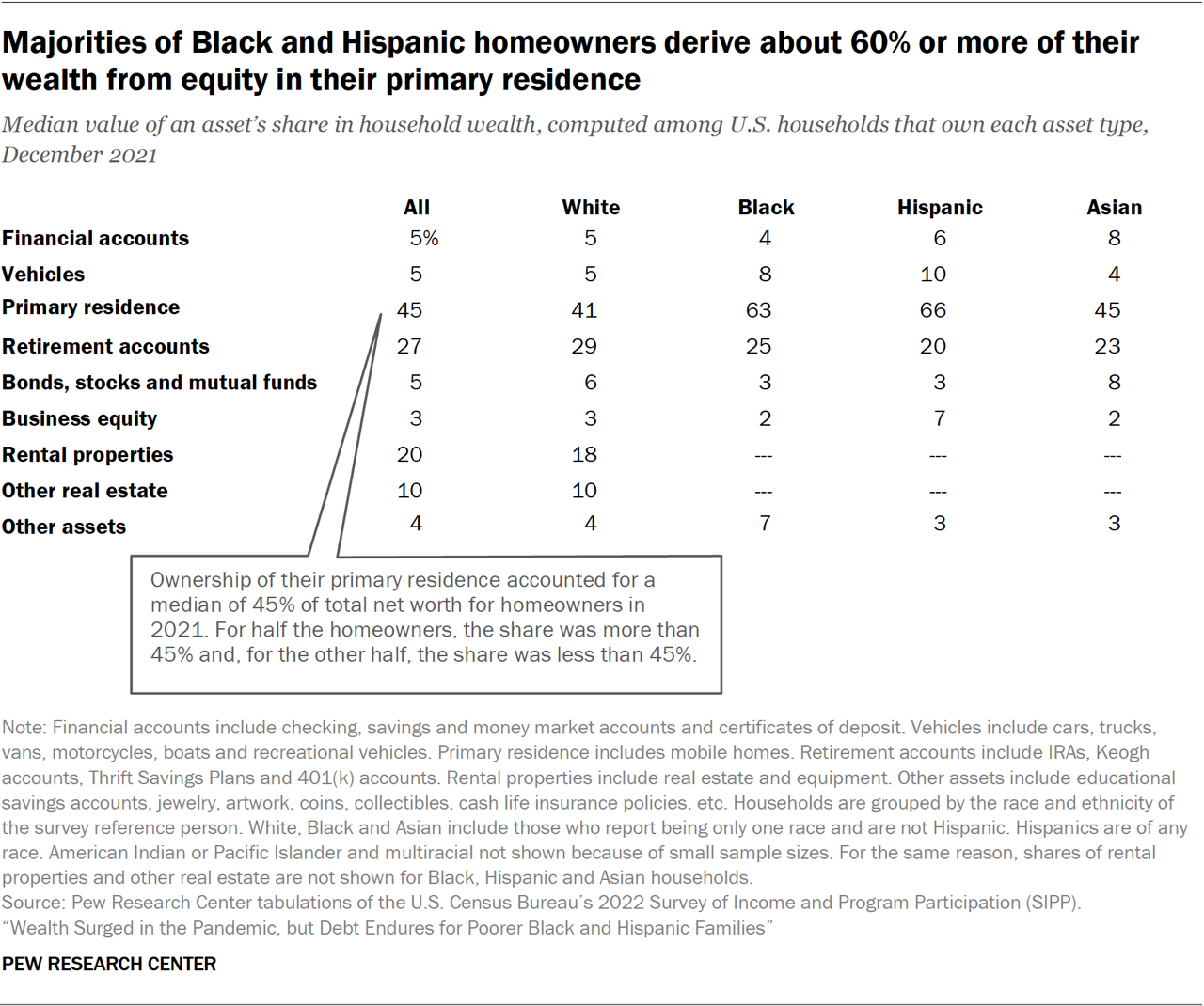

One more reason why a web value of 25X annual bills will not be enough to retire early is the excessive share of web value tied up in housing. In keeping with Pew Research, in 2021, the median web value of U.S. households stood at $166,900, together with all belongings, with dwelling fairness accounting for a median of 45% of this web value. The share is probably going comparable right now.

Nonetheless, when inspecting Pew’s article, they state, “In 2021, owners sometimes had $174,000 in fairness of their houses,” alongside the nationwide median web value determine of $166,900. This discrepancy suggests dwelling fairness might symbolize an even bigger share of web value for a lot of households.

Assuming 45% of 1’s web value is of their major residence is correct, that also leaves the everyday family with solely 55% of their web value in different belongings, corresponding to automobiles, monetary accounts, retirement funds, enterprise fairness, rental properties, and different actual property.

Taxable Brokerage Accounts: A Small Slice of Internet Price

Inside this remaining 55%, Monetary accounts—which I interpret as taxable brokerage accounts—make up a modest 5% for all races surveyed. Clearly, these accounts alone aren’t sufficient to maintain early retirement for many.

Curiously, Pew’s information reveals that for White households, rental properties and different actual property symbolize 30% of complete web value, indicating that many White Individuals generate rental earnings as landlords.

Maybe Pew’s survey pattern didn’t seize enough information from Black, Hispanic, and Asian households to mirror their possession of rental properties and different actual property. But, real estate is a favored asset class for a lot of Asians, together with myself.

However is a mixed 5% in monetary accounts plus 30% in rental properties and different actual property enough to generate livable passive earnings for early retirement? Realistically, it’s extremely unlikely.

So let’s be beneficiant. Let’s assume all the 55% of web value is 100% allotted to productive income-generating belongings like shares and actual property. What would the extra reasonable web value goal primarily based on annual bills be?

45.5X Annual Bills Might Be A Extra Cheap Goal For The Typical Family

Making use of some primary math, with solely 55% of the everyday American family’s web value exterior of their major residence, the everyday family would wish a web value equal to 45.5X annual bills to attain early retirement.

I can already hear the complaints from readers saying {that a} 45.5X annual bills goal is each unrealistic and demoralizing. But when the info in regards to the typical net worth composition of Individuals is correct, then this goal is grounded in simple arithmetic.

To know why, think about if 100% of your web value had been tied up in your major residence. Each bed room is occupied, and you’ll’t hire out any a part of the home for earnings. How would you fund your retirement with such a web value composition? Even when your own home had been value 100X your annual bills, it wouldn’t aid you cowl your residing prices until you took out a House Fairness Line of Credit score (HELOC), did a cash-out refinance, or carried out a reverse mortgage.

In early retirement, you want to depend on passive earnings or liquidating belongings to cowl your bills. In conventional retirement, Social Safety advantages and pensions present extra assist, lowering the reliance on these methods.

Letting Go of a Strict Definition of Monetary Independence and Withdrawing Extra

A ultimate strategy to the 25X annual bills debate is to let go of a inflexible definition of FIRE: your investments generate sufficient earnings to cowl your residing bills. As a substitute, construct a web value of no less than 25X your annual bills and easily withdraw at a 4% (or probably increased) price, no matter what anyone thinks.

Bill Bengen’s 4% rule, established in his 1994 research, assumes retirement at age 65. Bengen discovered that retirees starting at this age may safely withdraw 4% of their retirement portfolio within the first yr, then alter yearly for inflation, anticipating the portfolio to final for no less than 30 years—till age 95—with out working out.

In case you plan to retire at 65, you could possibly confidently withdraw at a 4% price or perhaps a 5% price, as Invoice now suggests. Nonetheless, if you would like your wealth to endure for generations, think about decreasing your secure withdrawal price to make sure the sustainability of your monetary legacy.

Key level: For these nonetheless making an attempt to determine how a lot to build up, you should calculate the share of your web value in productive belongings after which decide a correct a number of of bills to provide you with a web value goal.

For instance, if the baseline goal web value a number of of annual bills is 25, then divide 25 by the share of your web value in liquid, income-producing belongings to get your extra reasonable goal a number of.

Formulation to Calculate Your True Annual Expense A number of Wanted to Retire Early

To find out the true a number of of your annual bills wanted to retire early, you’ll have to assess two key elements:

- The minimal annual expense a number of you consider is important for early retirement.

- The share of your web value held in income-producing, liquid investments.

Right here’s the way it works:

Let’s assume you consider {that a} web value of 25X your annual bills is enough for early retirement. Nonetheless, solely 70% of your web value is in income-producing, liquid investments. To regulate for this, you should utilize the next system:

True Annual Expense A number of = Baseline Annual Expense A number of ÷ Share of Internet Price in Earnings-Producing, Liquid Investments

For this instance:

True Annual Expense A number of = 25 ÷ 0.7 = 35.7

If 70% of your web value is in income-producing, liquid belongings, you would wish a web value of 35.7 occasions your annual bills to attain the identical monetary safety as somebody with 100% of their web value in such belongings.

It’s because the 30% of non-liquid, non-income-producing belongings will not contribute on to producing earnings for bills, so that you want a better total web value to compensate. After all, as you modify your web value composition, you possibly can re-calculate your true annual expense a number of for early retirement.

Concentrate on Constructing Internet Price First, Then Money Move

If you wish to retire earlier, logically, you should discover a technique to obtain a web value goal equal to your true annual expense a number of sooner. This normally requires working longer, saving extra, and taking up extra threat.

Additional, the federal government taxes earnings extra closely than funding good points, making it extra advantageous to prioritize rising your web value over producing money move within the early levels of your monetary journey. Whereas there’s ongoing debate a couple of potential wealth tax, it’s unlikely to turn into a actuality anytime quickly.

Solely while you’re able to cease working completely or your lively earnings sources considerably dwindle ought to producing passive earnings take heart stage.

In our case, my spouse and I don’t have conventional jobs, but we stay aggressive buyers. Monetary Samurai, our “X Factor,” gives supplemental earnings that we didn’t totally anticipate once we left our company roles in 2012 and 2015. This extra earnings has allowed us to tackle extra funding threat, corresponding to specializing in growth stocks and allocating capital to venture funds for personal market publicity.

As we’ve elevated our investments in illiquid belongings, the trade-off has been slower passive earnings progress. Someday, Monetary Samurai will come to an finish, and when that point arrives, we’ll pivot to prioritize liquidity and income-generating investments. For now, the technique of constructing web value first permits us the pliability to pursue alternatives whereas preserving future money move in thoughts.

Do not Take The 25X A number of For Monetary Independence At Face Worth

Simply as focusing solely on income as a substitute of revenue can mislead in evaluating a enterprise, so can assuming that 25X annual bills is all one wants for monetary independence. Many individuals have web value tied up in houses, progress shares, personal firms, or collectibles that don’t generate earnings.

Based mostly on my early retirement expertise and that of others pursuing FIRE since 2009, a web value equal to 25X bills typically doesn’t actually present monetary independence. You’ll probably end up nonetheless working or in search of new earnings sources.

To really feel genuinely free, think about aiming for 40X bills or 20X your common gross earnings over the past three years. Higher but, do the straightforward math as I proposed in my system above. Whereas these net worth targets could seem bold, don’t underestimate the facility of compound returns and disciplined saving.

In case you don’t attain these multiples, that’s okay too. Many individuals proceed to earn lively earnings to fund their life-style targets. However now, I am much more emboldened by these targets because of information from Pew Analysis.

I’ve all the time felt these web value benchmarks had been reasonable primarily based on my observations. And now, with this nationwide information, my instincts are validated.

Reader Questions And Strategies

Readers, do you assume a web value equal to 25X your annual bills is sufficient to retire early on? Have you ever ever met somebody who did retire early on 25X bills and does not generate any lively earnings?

Free monetary checkup and $100 reward card: In case you have over $250,000 in investable belongings, take benefit and schedule a free session with an Empower financial professional here. Full your two free video calls with the skilled by November 30, 2024, and you may obtain a free $100 Visa reward card. There is not any obligation to make use of their companies after.

With a brand new president in workplace, it’s a good time to get a second opinion in your portfolio positioning. Consulting a monetary skilled in 2013 helped me develop my web value by an extra $1 million. If I met with one right now, I’m certain they’d suggest a extra balanced portfolio. However I’m a risk-taker at coronary heart.

The assertion is supplied to you by Monetary Samurai (“Promoter”) who has entered right into a written referral settlement with Empower Advisory Group, LLC (“EAG”). Click on here to be taught extra.